As a system (AGT is what I call my system) that trades intraday, its no surprise that it performs well in times of volatility where the intraday range expands, which is what typically happens during bearish times.

So it has got a bit of an insurance mechanism built-in to protect from Black Swans. But unlike the techniques employed by funds like Universa, AGT is not too shabby during uptrends either.

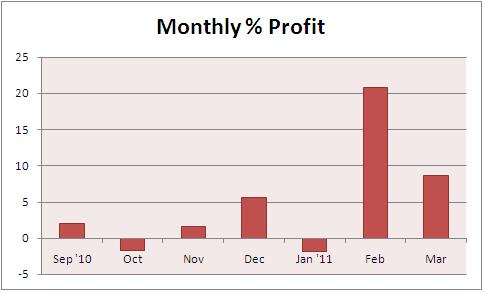

The peak of the GFC, which is from September 15th 2008 (Lehman Brothers collapse) until March 9th 2009 which was the bottom, when the VIX went crazy, is also the time AGT went nuts, and tacked on 83% in under 6 months.